Tokenization and Regulations: Insights from the Frontlines

To my normies and degen readers, don’t we all agree it’s a bright new day in America? (Not too bright in Boston though).

In the last few weeks, I’ve engaged with some of the most dynamic discussions shaping the future of digital finance—Consensus 2025, the SEC’s Task Force Roundtable on tokenization, and Harvard’s Blockchain Conferences. It is clear that the industry is experiencing a clear inflection point: stablecoins, yield-bearing assets, and tokenized real-world assets are no longer niche experiments—they’re becoming foundational to global market infrastructure. In my analysis below, I unpack the common threads—starting with the latest narrative shifts, moving into key regulatory movements and broader macro reflections.

1. The Latest Top Narratives

I. RWA Tokenization

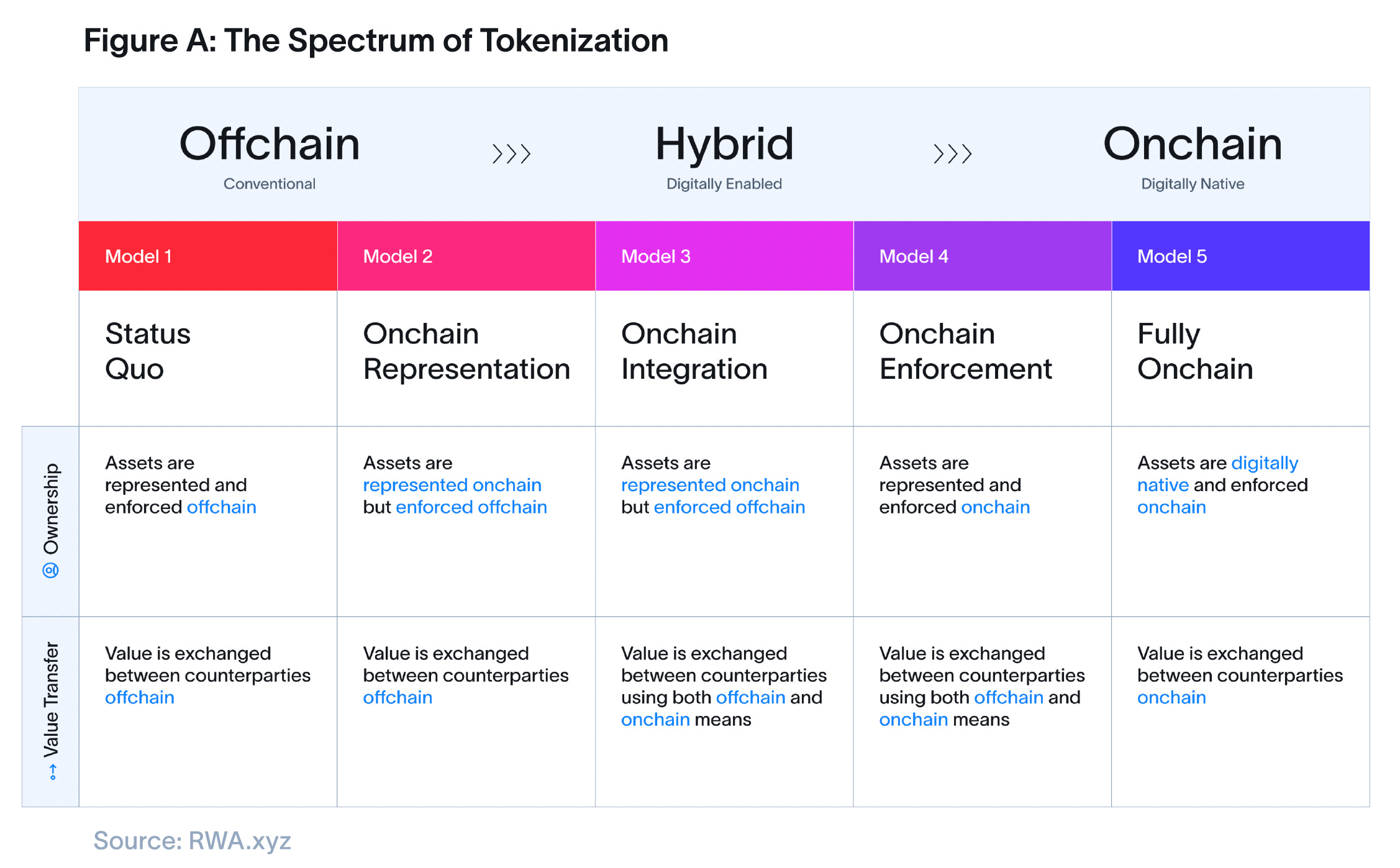

The concept of tokenization remains variably defined across the industry. As a working definition, I consider tokenization to involve the creation of digital representations of RWA that incorporates registered ownership and embedded programmability, thereby facilitating functionalities such as real-time compliance enforcement and automated dividend payments. In this regard, tokenization is not just a “wrapper”, but an enhancement that enables automated execution via embedding smart contracts. As outlined in RWA.xyz’s Report, tokenization is a spectrum but not a binary state.1

Stablecoins may have led tokenization’s first wave, but the market is rapidly evolving to bring more financial instruments onchain, such as money market funds (MMFs), private credits, repurchase agreements. Institutions are increasingly embedding tokenization into their legacy infrastructure to unlock liquidity, enhance composability and streamline settlement workflows. Notably, many of these initiatives have been utilizing public blockchains such as Ethereum and Solana. Recent examples include BlackRock’s tokenized MMF BUIDL and Etherfuse’s tokenized CETES.

I am particularly drawn to two trends:

(i) RWA tokenization introduces a pathway to generate liquidity independent of centralized moneymakers, especially in defi, by enabling a more direct relationship between issuers and stockholders and minimizing the costs and frictions of involving intermediaries;

(ii) The collateralization of MMFs: e.g. Ethena Labs’s BUDIL-backed USDtb, as well as with other instruments Wall Street are used to.

II. Stablecoins

Companies are racing to bring stablecoins mainstream. The proliferation of stablecoins—both in issuance and adoption—offers a critical lesson for legacy payment providers. Beyond serving as a mechanism for dollar buying, stablecoins are increasing positioned as a tool for cross-border remittance and a great value transfer mechanism replacing payment systems such as SWIFT. In particular, stablecoins are becoming key proxy in inflation-prone economies such as Argentina, Venezuela. Pegged 1:1 to USD, they present a more stable alternative to Bitcoin.

Stablecoins exemplify tokenization in practice, particularly through speeding up settlement from T+1 to T+0. However, as noted by Commissioner Crenshaw in the Roundtable, the increased efficiency raises a fundamental question:

Q: Whether the removal of settlement delay will remove key market protections altogether?

A: While T+0 settlement does reduce counterparty risk, the current delays accommodate key functions such as netting, fraud checks, and liquidity management—critical safeguards for market integrity. Hence, any shift to on-chain infrastructure must balance efficiency with these protections. More broadly, this tension reflects the underlying challenge of reconciling DeFi’s permissionless architecture with the need for on-chain KYC/AML compliance.

As signalled by the rise in stablecoins issuance, the narrative is no longer about crypto speculation, but about fiat utility. The rise of non-yield-bearing stablecoins adoption underscores that the demand is not just for yields, but for accessibility and reliability.

If tokenized U.S. treasuries are the world’s savings account, then stablecoins are the world’s checking account.

From a geopolitical perspective, stablecoins is a key to preserving USD dominance. Against the backdrop of intensifying U.S.-China competition, the real contest is over which nation builds the better infrastructure rails to integrate its currency into CeFi and DeFi ecosystems. In this context, stablecoins policy is closely intertwined with the country’s reserve currency status. It is also essential to distinguish between central bank digital currencies (CBDCs) with stablecoins. If stablecoins is considered as a creature of crypto, which centers on being permissionless and having sovereignty, then CBDCs can be seen as against such ethos. For instance, Wyoming’s state-issued stabletokens (WYST), which is fully backed by U.S. treasury bills, are not CBDCs and should be more accurately considered as a money transmission instrument.

II. The Explosion of Yield-Bearing Stablecoins

The premise behind YBS is intuitive: if users are effectively holding deposits, they should be entitled to earn yield on them. Currently, under the proposed stablecoin regulations in the U.S., stablecoin issuers are prohibited from offering YBS. Arguably, similar with instruments like MMF, YBS may be considered as security. This also raises a practical question:

Q: Why should investors opt for YBS over MMFs?

A: While it is true that this is a risk investors will have to price in, the answer likely lies in accessibility and flexibility. MMFs often require minimum investment thresholds, impose lock-up periods, and lack 24/7 tradability. In contrast, YBS offers collateral mobility, liquidity and 24/7 trading. The next frontier lies in developing solutions that allow retail to use yields generated from YBS.

2. Key Regulatory Movements

I. Why Regulation Matters

Perfect is the enemy of the good.

Any regulatory clarity will be beneficial to the industry—not only when it comes to providing opportunity for traditional infrastructure to innovate and rescale, but also broadening the TAM for blockchain and crypto adoption. Regulatory harmonisation is equally crucial.

II. Macro Regulatory Landscape

The current shift is notable. Under the new administration:

Banking regulators like the OCC and FDIC have reversed hostile crypto policies, reaffirming that banks can participate in stablecoin activities and custody digital assets. This stands as a clear retract from the choke point 2.0 during the Biden Administration.

Enforcement is pivoting away from intermediaries and towards actors involving in fraud and manipulation. The SEC’s Crypto Taskforce has been organizing roundtables and in the Roundtable last Monday, Chairman Atkins highlighted that the SEC will act eventually and that the current staff pronouncements are just temporary, noting the need for additional guidance and registration exemptions. One panellist in Consensus noted an apparent contradiction: if the SEC is not enforcing, this renders any exemptive reliefs nugatory.

III. The GENIUS Act (“Guiding and Establishing National Innovation for U.S. Stablecoins Act”)

The GENIUS Act2 has the potential to become landmark legislation for stablecoins. My brief analysis:

The Act defines “payment stablecoins” as digital assets pegged to a fixed monetary value, used or designed to be used as a means of payments or settlement;

The Act sets standards for reserves and disclosures, and, critically, it resolves bankruptcy risks. In the wake of collapses like Terra Luna, the Act would prioritize stablecoin holders above other creditors;

Only “permitted payment stablecoin issuers” may issue stablecoins in the U.S. Notably, issuers with over $10b in market value must register federally, and these federal qualified issuers may comprise of nonbank entities approved by the OCC. That said, some players are contemplating to obtain the bank license/charter, even though they are technically not required under the Act. Why? Likely to send strong compliance signal to investors, and perhaps to directly use the Federal Reserve Bank master account to buy treasuries, cutting out custodial banks or asset managers, such as those managing Circle Reserve Fund;

One major loophole is with regards to the treatment of foreign issuers:

The current version of the Act requires the foreign issuer of stablecoins (i) to be coming from a comparable jurisdiction; (ii) to have registered with the Comptroller; and (iii) to comply with U.S. lawful orders;

However, with the Democrats’ recent markup, the bar has been raised: foreign issuers must now register with U.S. regulators.3 This move is arguably targeted towards one of the largest offshore stablecoin players and/or combat a potential “crypto Eurodollar” issue, whereby runs-on offshore stablecoins can destabilize U.S. treasury markets;

It is also a sharp contrast to foreign frameworks such as Hong Kong’s Stablecoin Bill, which requires foreign issuers providing services to retail in Hong Kong to obtain a license4;

Crypto regulations may be moving from a bipartisan issue to a political one, again: Democrats voted down the GENIUS Act last week, citing concerns over potential Trump-affiliated financial interests. In particular:

The launch of USD1 by Trump-linked World Liberty Financial, which was used to close the $2bn investments by Abu Dhabi-based MGX into Binance;5

Alleged self-dealing and conflict of interests issues concerning Trump’s family’s crypto involvement. Data from Chainalysis allegedly shows that the creators of the TRUMP token made $320mn in fees.6

However, there are also legislative pushback— acts as the End Crypto Corruption Act block all members of Congress, the president, vice president, other executive branch officials and their families from “issuing, endorsing or sponsoring crypto assets.”7 Still, one should ask: shouldn’t the President have the right to engage in crypto, just as any other American citizens?

The upshot? Compared with the Market Infrastructure Bill, GENIUS Act is relatively simple. Passing it will send a strong signal to the industry.

IV. Market Infrastructure Bill

Progress here is slower, but potentially more transformative. This Bill will define the division of regulatory oversight between the SEC and CFTC. If stablecoin legislation stalls, this too risks delay. Notably, regulators note the difficulty in understanding the Bill given the technicalities therein. I’ll be unpacking that in a separate post—there’s too much nuance to do it justice here.

3. Potential Global Headwinds

1. Tariff Tensions

Tariffs are injecting uncertainty into global flows. They are inherently value-destructive and raise risk premiums across markets. In this environment, crypto has been one of the few asset classes showing strength, particularly as traditional markets stagnate. However, I query whether the tariff war will dampen USD usage and subsequently, demand for USDC.

2. Interest Rate Dynamics

Stablecoins are pegged with fiat and backed by assets like the U.S. treasuries, making stablecoin yield closely correlated with interest rates. This exposure has a clear downside in the face of a looming recession: if rates fall, yield-bearing instruments become less attractive. That said, lower rates also reduce the opportunity cost of holding USDC, potentially increasing its circulation. Predicting the net effect remains challenging. A broader question is whether stablecoin revenue will continue to rely on traditional interest-bearing reserves or shift towards active portfolio management by chartered institutions.

https://22049776.fs1.hubspotusercontent-na1.net/hubfs/22049776/RWA.xyz%20-%20The%20Spectrum%20of%20Tokenization.pdf

https://www.congress.gov/bill/119th-congress/senate-bill/394/text [photo credits: https://www.bloomberg.com/news/articles/2025-03-07/trump-signs-order-creating-bitcoin-reserve-and-crypto-stockpile]

https://www.galaxy.com/insights/research/genius-act-stablecoin-regulation

https://www.legco.gov.hk/yr2024/english/bills/b202412064.pdf

https://www.reuters.com/world/middle-east/wlfs-zach-witkoff-usd1-selected-official-stablecoin-mgx-investment-binance-2025-05-01/

https://www.coindesk.com/business/2025/05/09/trump-family-profited-usd320m-on-memecoin-despite-87-decline-since-day-one

https://www.merkley.senate.gov/wp-content/uploads/End-Crypto-Corruption-Act.pdf